For a market with an atomless continuum of assets, we formulate the intuitive idea of a ''well-diversified'' portfolio, and present a notion of ''exact arbitrage'', strictly weaker than the more conventional notion of ''asymptotic...

moreFor a market with an atomless continuum of assets, we formulate the intuitive idea of a ''well-diversified'' portfolio, and present a notion of ''exact arbitrage'', strictly weaker than the more conventional notion of ''asymptotic arbitrage'', and necessary and sufficient for the validity of an APT pricing formula. Our formula involves ''essential'' risk, one based on a specific index portfolio constructed from factors and factor loadings that are endogenously extracted to satisfy an optimality property involving a finite number of factors. We illustrate how our results can be translated to markets with a large but finite number of assets. r , pp. 173-197] for a discussion of naive and efficient diversification. We note here that there is no uniform terminology in the literature. For example, the terms non-diversifiable risk and diversifiable risk used here for the CAPM are also called systematic risk and unsystematic risk in . On the other hand, systematic risk and unsystematic risk used here for the APT model are also referred to as non-diversifiable and diversifiable risk in, for example, [37,38, pp. 116-120].

![Figure 2: Optimal Predictor p(n) Under a Half-normal and a Triangular Distribution Evaluated at p = 0 and j = 1 for the triangular distribution on [0,1], this reduces to](https://figures.academia-assets.com/35408/figure_003.jpg)

![In this appendix we show that high risk aversion pushes the optimal price toward the mid- point of the support. In other words, if f(-) is without loss of generality right-skewed, then p(n) is increasing in n, Vn > 1. First, note that p(n), p(n) € |p, p], is continuous. If p or p are infinite, we replace these bounds with a function of n, thereby making the domain of p compact. As f(-) and all components of the integral are continuous functions, the theorem of the maximum gives continuity of p(n). Next, to evaluate how the optimal price p(n) responds to changes in risk aversion n, take](https://figures.academia-assets.com/35408/figure_009.jpg)

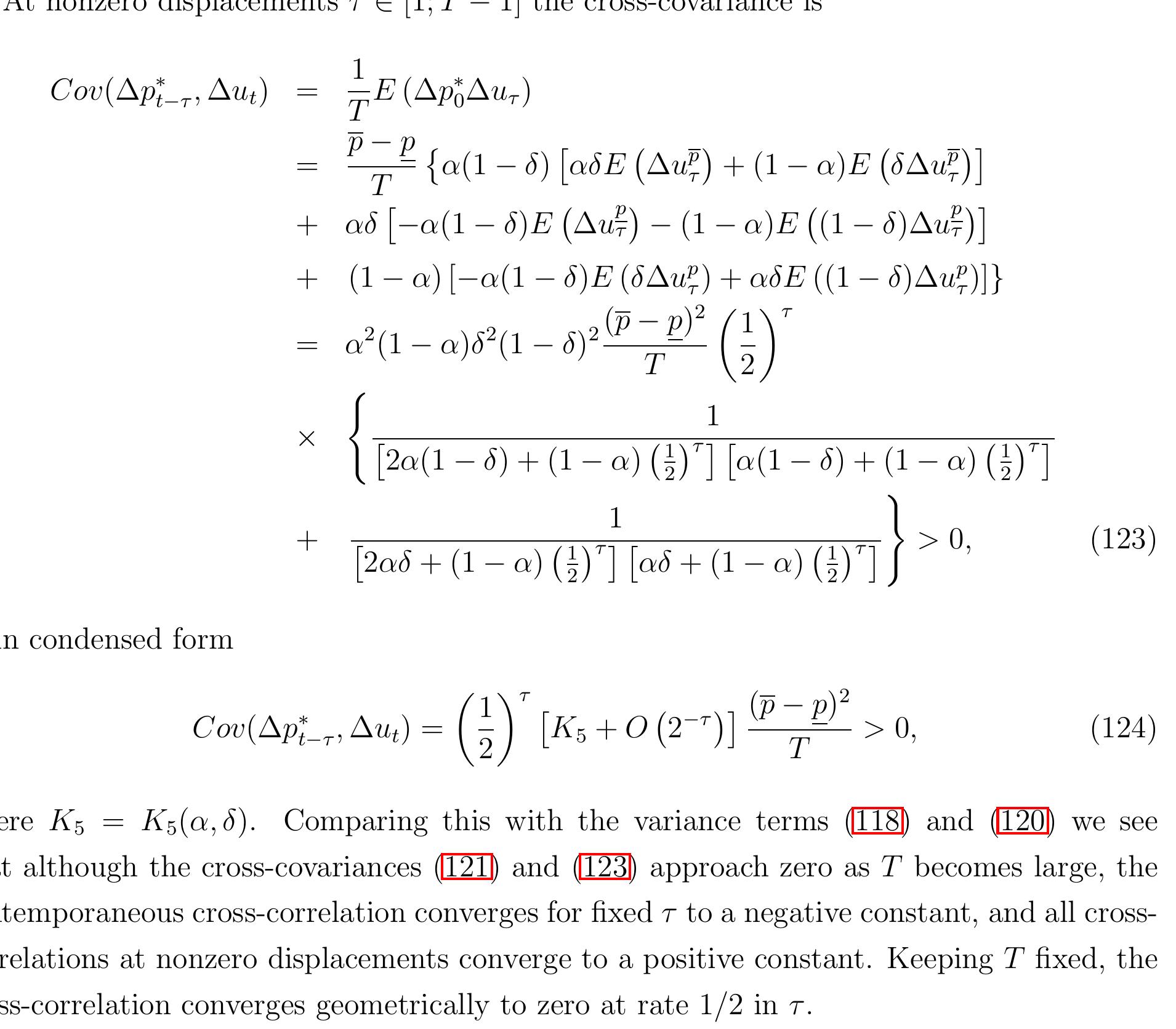

![In the multi-period setup of section [4.1] the semi-strong form efficient price has the uncondi tional variance ~ SI Semi-strong form Cross-correlations](https://figures.academia-assets.com/35408/figure_012.jpg)

![do not hold in general, but only for a quadratic market maker loss function. Proposition [8] shows that the size of the spread matters only relative to the adverse selection parameter. The cross-correlation at displacement one, for example, is negative if and only if the spread exceeds the adverse selection cost. s > A is reasonable, because the spread must cover the order processing cost. It also entails, however, that the average trader in expectation incurs a loss with every transaction. Hasbrouck (2007) justifies this with the liquidity needs of traders. The sign of contemporaneous cross-correlation is ambiguous in general. As in Diebold (2006), for s sufficiently large (and \\ > $E(q@é,)) the model predicts a cross-correlation pattern that is exactly the opposite of the empirical pattern in Hansen and Lunde (2006). We illustrate this in the last row of Figure [I] which on the left shows the cross-correlation function for a small spread (0 < s < \\), and on the right for a sufficiently wide spread (s > A > 0). If sufficiently many lags are included, the Hansen and Lunde estimator is unbiased for the strong form efficient price defined as in and (2), but by construction not for its semi-strone form counterpart.](https://figures.academia-assets.com/35408/table_002.jpg)

![Now that we have reduced the study of the distribution of the modulus of continuity to that of the maximum fluctuation over our constructed subintervals we can progress by introducing a maximal inequality. In order to do this we use the following known result taken from [6] and paraphrased for use here.](https://figures.academia-assets.com/30894152/figure_001.jpg)