A Beginner's Guide to Structural Equation Modeling, second ed., 2004, Lawrence Erlbaum and Associates, Mahwah, NJ Is structural equation modeling (SEM) a mathematical Godsend or an instrument of the devil? Well respected researchers have...

moreA Beginner's Guide to Structural Equation Modeling, second ed., 2004, Lawrence Erlbaum and Associates, Mahwah, NJ Is structural equation modeling (SEM) a mathematical Godsend or an instrument of the devil? Well respected researchers have staked a claim on each side of this debate, and I outline both positions briefly below. But no matter which stance one takes, SEM has acquired such a stature and prevalence in the social sciences that, for better or worse, evaluators of all stripes must come to grips with it. Even hard-core qualitative researchers who think statistical analysis is no more informative than numerology can benefit from an understanding of SEM. For example, consider reports of quantitative social science (such as that television viewing in infancy causes attention deficits in later childhood or that day-care fosters anti-social behavior) that frequently find their way to the front pages of the newspaper. Because such findings are often derived from SEM methods, a thoughtful critique requires an understanding of at least the rudiments of that methodology.

![This function also implausibly implies, as Pratt [17] and Arrow [1] have noted, that the insurance premiums which peo- ple would be willing to pay to hedge given risks rise progress- ively with wealth or income. For a related result, see Hicks (6, p. 802]. gs It is, consequently, very relevant to note that by using the Bienaymé-Tchebycheff inequality, Roy [19] has shown that investors operating on his “Safety First” principle (i.e. make risky in- vestments so as to minimize the upper bound of the probability that the realized outcome will fall below a pre-assigned “disaster level’) should maximize the ratio of the excess expected port- folio return (over the disaster level) to the standard deviation of the return on the port- folio?! — which is precisely our criterion of max 6 when his disaster level is equated to the risk- free rate r*. This result, of course, does not depend on multivariate normality, and uses a different argument and form of utility function. ML. Ci pee ntinea Mhaneneee nerdy 24n Onreweurlanwnn](https://figures.academia-assets.com/30555591/figure_001.jpg)

![The conclusions stated in the text are obvious from the graph of this case (which incidentally is formally identical to Hirschleifer’s treatment of the same case under certainty in [¥].)](https://figures.academia-assets.com/30555591/figure_002.jpg)

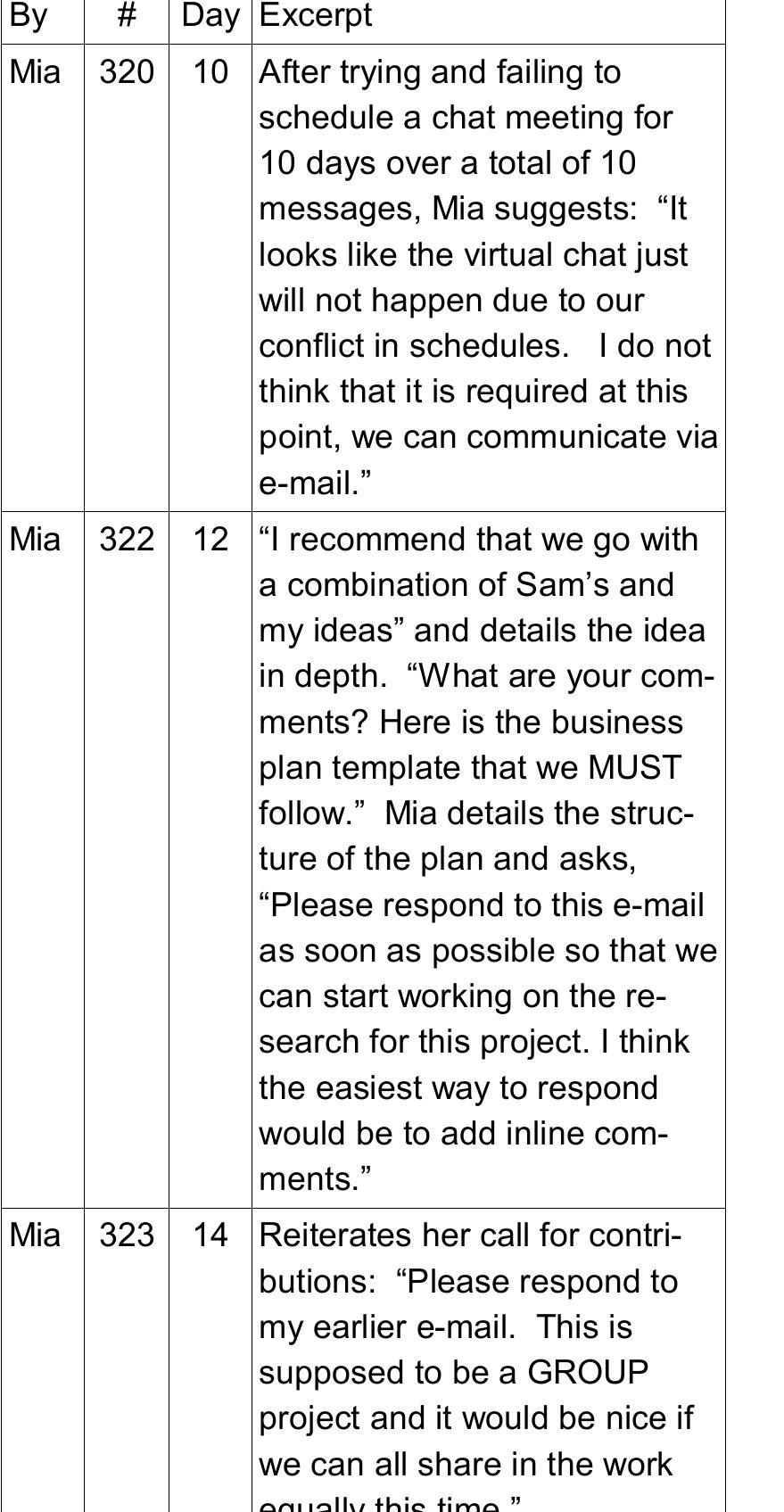

![As in Team 19T,,, this concern with deadlines leads to heightened vigilance and active moni- toring of teammates contributions by some members (e.g., “I have not received any feedback from anyone regarding the document | sent to you” [Art, 70]; “Ron, are you going to write the next progress reports?” [Art, 72; 74]; “Il checked the communication hub and there was no report so far submitted” [Ron, 90]).](https://figures.academia-assets.com/51339445/table_018.jpg)

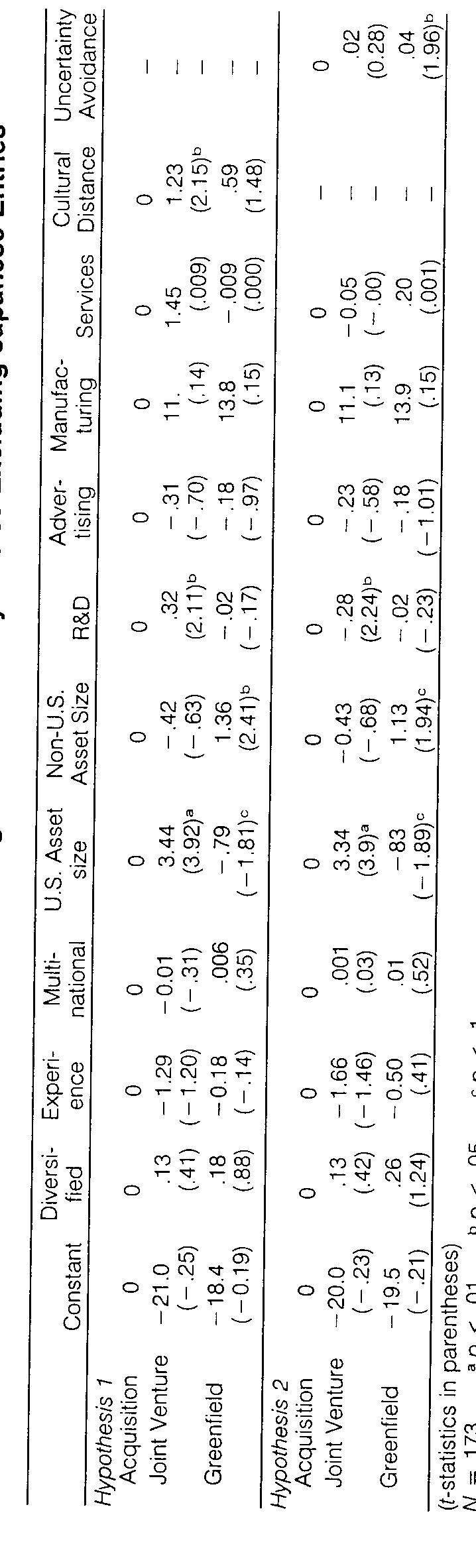

![Summary of Predicted Signs Uncertainty Avoidance [Uncertainty Avoidance].](https://figures.academia-assets.com/10381602/table_003.jpg)

![Table II. Equilibrium correction form of the ARDL(6, 0, 5, 4, 5)

earnings equation

Notes: The regression is based on the conditional ECM given by (30)

using an ARDL(6, 0,5, 4,5) specification with dependent variable, Aw;

estimated over 1972ql-— 199744, and the equilibrium correction term

H%-1 is given in (31). R is the adjusted squared multiple correlation

coefficient, G is the standard error of the regression, AI and Bae are

Akaike’s and Schwarz’s Bayesian Information Criteria, xXbc (4), XF 2 (1),

x7 (2), and x20) denote chi-squared statistics to test for no residual

serial correlation, no functional form mis-specification, normal errors and

homoscedasticity respectively with p-values given in [-]. For details of

these diagnostic tests see Pesaran and Pesaran (1997, Ch. 18).](https://figures.academia-assets.com/46980930/table_011.jpg)

![“Total Accruals (TA,,) is defined as the change in non-cash current assets minus the change in current liabilities excluding the current portion of long-term debt minus depreciation and amortization [with reference to COMPUSTAT data items, TA = (AData4 — ADatal — AData5 + AData34 — Datal4)/lagged Data6]. Discretionary accruals from the Jones model are estimated for each industry and year as follows: TAj, = % + %/ASSETS;;-1 + #2ASALES;, +a3PPE;, + &i, where ASALES,, is change in sales scaled by lagged total assets and PPE;, is net property, plant and equipment scaled by lagged assets. Discretionary accruals from the modified-Jones model are estimated for each industry and year as for the Jones model except that the change in accounts receivable is subtracted from the change in sales. Discretionary accruals from the Jones Model (Modified-Jones model) with ROA are similar to the Jones Model (Modified-Jones model) except for the inclusion of current or lagged year’s ROA as an additional explanatory variable. For performance matched discretionary accruals, we match firms on ROA in period ¢ or t—1. To obtain a performance-matched Jones model discretionary accrual for firm i we subtract the Jones model discretionary accrual of the firm with the closest ROA that is in the same industry as firm i. A similar approach is used for the modified Jones aaa nAdal](https://figures.academia-assets.com/49093162/table_003.jpg)

![“Discretionary accruals from the Jones model are estimated for each industry and year as follows: TA;; = % + «;/ASSETS;;_; + #ASALES,;, + 03PPE;, + &, where TA;; is defined as the change in non-cash current assets minus the change in current liabilities excluding the current portion of long-term debt minus depreciation and amortization [with reference to COMPUSTAT data items, TA = (AData4 — ADatal — AData5 + AData34 — Data14)/ lagged Data6]. ASALES;, is change in sales scaled by lagged total assets (ASSETS; ;_1), and PPE;, is net property, plant and equipment scaled by ASSETS, ,_1. Discretionary accruals from the Jones Model (Modified-Jones Model) with ROA are similar to the Jones Model (Modified-Jones Model) except for the inclusion of current or lagged year’s ROA as an additional explanatory variable. For performance matched discretionary accruals, we match firms on ROA in period ¢t or t—1. To obtain a performance-matched Jones model discretionary accrual for firm i we subtract the Jones model discretionary accrual of the firm with the closest ROA that is in the same industry as firm i. A similar approach is used for the modified Jones model.](https://figures.academia-assets.com/49093162/table_012.jpg)

![“Discretionary accruals from the Jones model are estimated for each industry and year as follows: TA;; = % + «/ASSETS;;-1 + #ASALES,;; + a3PPE;, + &, where TA;, (Total Accruals) is defined as the change in non-cash current assets minus the change in current liabilities excluding the current portion of long-term debt minus depreciation and amortization [with reference to COMPUSTAT data items, TA = (AData4 — ADatal — AData5 AData34 — Data14)/lagged Data6], ASALES;, is change in sales scaled by lagged total assets (ASSETS;,_;), and PPE;, is net property, plant and equipment scaled by ASSETS,,_;. Discretionary accruals from the Jones Model (Modified-Jones Model) with ROA are similar to the Jones Model (Modified-Jones Model) except for the inclusion of current or lagged year’s ROA as an additional explanatory variable. For performance matched discretionary accruals, we match firms on ROA in period t or t—1. To obtain a performance-matched Jones model discretionary accrual for firm i we subtract the Jones model discretionary accrual of the firm with the closest ROA that is in the same industry as firm 7. A similar approach is used for the modified Jones model. Panel B. Ha: Accruals > 0* (Figures in bold (old italic) signify rejection rates that are significantly exceed (fall below) the 5% nominal significance level test and indicate that such tests are biased against (in favor of) the null hypothesis)](https://figures.academia-assets.com/49093162/table_007.jpg)